Outlook

The outlook for Asian Real Estate Securities continues to be shaped by two overarching concerns: interest rates and Middle East tensions, with the latter sustaining supply chain disruptions that keeps inflation elevated across the region. Asian equity markets have nonetheless performed strongly, carried by technology and semiconductor names that constitute large index weights, alongside banks benefiting from wider net interest margin spreads. In the meantime, real estate stocks have been left behind. Real estate fundamentals across the region remain sound, with healthy leasing activity and limited new supply in many markets and sectors, yet investor apathy toward the rate-sensitive sector has driven meaningful underperformance. Some relief on the interest rate and inflation outlook is necessary to see a sustained recovery, and we remain constructive on the sector given the underlying fundamentals.

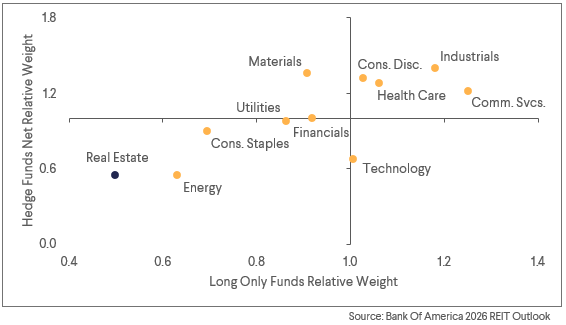

Bank of America Investor Sentiment

June 16th is the critical near-term date for Asian real estate investors, with both the BOJ and RBA announcing rate decisions simultaneously. In Japan, we expect a hike despite May's softer Tokyo CPI print, as the BOJ has been explicit that real rates remain deeply negative and further normalization is warranted. The statement's guidance on the pace of subsequent hikes will matter as much as the decision itself. In Australia, the RBA has now raised rates three times in 2026, fully reversing the three cuts delivered in 2024-25. A pause is the base case: the latest monthly CPI showed improvement, and the labor market has shown signs of softening, though trimmed mean inflation remains well above the target band.

Japan

Tokyo's core CPI came in at 1.3% YoY which was well below consensus at 1.5%. More importantly, core-core (stripping out energy and food which have been suppressed by subsidies) came in at 1.6% vs expected 1.9% which was the April read. Core-core is the BOJ's preferred gauge and Tokyo CPI tends to lead the national averages meaning that this does show some price deceleration. This doesn't change our view that the BOJ will hike in June and perhaps later this year. It does perhaps help the outlook for longer duration assets now that real yields are firmly positive. Developers and JREITs continue to struggle as JGB yields have headed higher. Ironically, cap rates remain very firm and transactions remain active. One potential near-term catalyst for the sector that will illustrate price discovery at scale is the sale of Fuji Media's non-core real estate business, driven by activist investors. The bidding process for Fuji Media's real estate subsidiary, Sankei Building Co., has drawn bids exceeding ¥1 trillion ($6.3bn), making it the largest property transaction in Japanese history. The portfolio, anchored by the 31-storey Tokyo Sankei Building in Otemachi, also encompasses hotels, apartments, and logistics assets, with total assets of ¥613bn on the balance sheet, implying a 60%+ premium to book at current bid levels. More than 15 firms submitted first-round bids, including KKR, Blackstone, Goldman Sachs, Mitsubishi Estate, and Mitsui Fudosan, signaling the depth of both domestic and foreign capital targeting prime Tokyo real estate. The deal is a direct product of TSE governance reform pressure on Japanese conglomerates to divest non-core assets, and a transaction at these levels would establish a definitive cap rate benchmark for Grade-A Tokyo office while accelerating a broader wave of corporate real estate monetization across the market. While this event alone is not enough to turn sentiment, we do remain optimistic that current Developer and JREIT valuations are mispriced and offer good risk return profiles for medium term investors.

Australia

The RBA meeting on June 16 is unlikely to bring much clarity regarding the future direction of interest rates. Inflation continues to run above the RBA's target and, unlike the Fed, the RBA does not have a dual mandate covering employment, so weaker job numbers alone will not force its hand. The April monthly CPI print came in at 4.2% year-on-year, down from 4.6% in March, giving the RBA sufficient cover to pause, though trimmed mean inflation at 3.3% remains well above their 2–3% target band. Three of the four major banks now see 4.35% as the peak for this cycle, with NAB shifting to that view on June 9 after GDP data and its own business survey showed slowing momentum; CBA, NAB and ANZ see the next move as a cut, most likely in 2027. Westpac remains the outlier, still forecasting two further 25bps hikes to 4.85%. A confirmed rate peak would be a direct positive for residential developers Mirvac and Stockland, where the key earnings driver is settlement volumes and lot sales, both of which are acutely sensitive to mortgage affordability and buyer confidence. The 2026 Federal Budget's negative gearing reform, restricting tax deductions for only new builds from July 1, 2027, is an additional structural tailwind, redirecting investor demand toward new supply and supporting the pipeline of both names. Should the higher-for-longer scenario prevail, Goodman offers relative defensiveness within the sector, with data center development now representing 73% of work-in-progress and earnings largely insulated from domestic rate sensitivity. Given the correction AREITs started well before the war in Iran, and since its relative severity was much greater than in other markets, we see potential for a stronger rally in Australia if an RBA pause is followed up with softer macro data. Valuations in some cases have reverted to 2022 levels when interest rate increases were only starting and debt costs were coming off pandemic lows.

Hong Kong

Hong Kong real estate securities have outperformed year-to-date on strengthening residential sales led by end user and investor demand, the bottoming of Central Office market trends, and improving luxury retail sales. Chinese buyers set a record HK$43bn ($5.5bn) in Hong Kong residential purchases in Q1 2026, a major driver behind the market's recovery and the basis for major bank forecasts of 10–15% price growth for the year. Beijing's decision in May to tighten enforcement of capital outflow rules, with SAFE introducing stricter monitoring of cross-border fund movements and enhanced identity verification at mainland banks, has worried investors that this demand could be put at risk. It should be noted that while Mainland buyers represent a large portion of the buying, many of them are residents of HK or have HK IDs. JPMorgan estimates that buyers that don't have HK ID's only represented 5.5% of the volume and 7.2% of the value. Home purchases using company structures made up only 4.5%. While capital controls may impact the property market and stock market temporarily, mid-end residential demand will be supported by population growth and rental yields. We will be looking at Q2 transaction data due in July for a read on whether the stricter enforcement is having any impact on residential volumes.

Singapore

With no MAS meeting until October, there is no policy impact from the Central Bank. Back in April, the MAS announced a tightening in response to higher oil prices which translates into a stronger NEER appreciation of the SGD rather than an increase in base rates. Rates, while drifting higher recently, are very low with 3-month SORA at 1.06%. Despite recent office transactions and solid rental growth for retail landlords, SREITs remain lackluster despite reasonable yields and moderate growth. Like elsewhere in the region, we think a catalyst for the sector needs to come from outside. A drop in crude oil and less hawkish Central Banks would likely be the trigger, however it is not likely until there is a resolution of the war in Iran. We remain bullish on retail, office and DC exposure in Singapore. City Developments (CDL) is approaching a critical juncture, with the outcome of its strategic review, initiated at the FY2025 results briefing in February and conducted by advisor Teneo, due by end of June. The review is centered on capital recycling, with analysts identifying SGD 6-7bn of non-core assets as disposal candidates, building on the SGD 2bn of divestments already executed in 2025. The return of Kwek Leng Peck as Vice Chairman from June 1st, bringing the founding family back into an active governance role precisely as the review concludes, signals that the family intends to be directly involved in directing the portfolio repositioning. A credible and ambitious outcome from the review would be a meaningful re-rating catalyst for the stock, which trades at a material discount to NAV.

Download the PDF version of the report here